Is Term Life Insurance Worth the Investment for Your Family's Future?

When considering whether term life insurance is worth the investment for your family's future, it's essential to evaluate your financial situation and long-term goals. Term life insurance offers a death benefit that can provide your loved ones with financial security in the event of your passing—replacing lost income, covering outstanding debts, and funding future expenses such as your children's education. This type of policy is often more affordable than whole life insurance, making it accessible for families looking to ensure financial stability without breaking the bank.

Moreover, term life insurance can be tailored to specific needs over a defined period, typically ranging from 10 to 30 years. This flexibility allows policyholders to align their coverage with significant life events, such as purchasing a home or raising children. In many cases, families find peace of mind knowing that they can depend on this safety net. Ultimately, while it may not be a traditional investment, the value of term life insurance lies in the protection and financial confidence it can provide, making it a worthy consideration for safeguarding your family's future.

Understanding the Benefits of Term Life Insurance: Peace of Mind for You and Your Loved Ones

Understanding the Benefits of Term Life Insurance can provide individuals and families with a sense of security that is hard to quantify. Unlike other forms of insurance, term life insurance typically offers a straightforward, affordable solution for those looking to protect their loved ones from financial hardship in the event of an unexpected loss. By selecting a specific term, policyholders can ensure that their beneficiaries receive a tax-free payout, which can cover anything from daily living expenses to educational costs. This peace of mind allows individuals to focus on enjoying life without constantly worrying about what would happen in their absence.

Moreover, term life insurance is highly flexible, making it an ideal choice for various needs and stages of life. For example, young families may prefer a policy that covers them during crucial years, while those approaching retirement may opt for a shorter term to ease financial burdens as they transition into a new phase. With options such as renewable or convertible policies, individuals can adjust their coverage as their circumstances change. Ultimately, investing in term life insurance is not just about the financial support it provides; it is also about fostering peace of mind for you and your loved ones, knowing that they will be taken care of no matter what happens.

Term Life Insurance vs. Other Policies: Which is Best for Your Family's Needs?

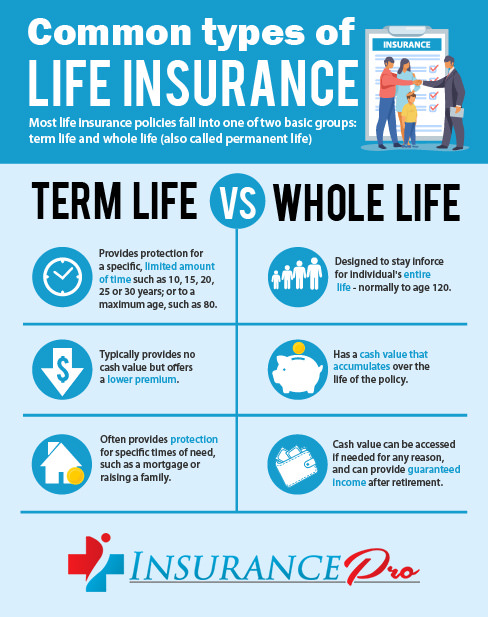

Term life insurance is often considered a straightforward option for families looking to provide financial security during specific periods, such as raising children or paying off a mortgage. Unlike permanent policies, which can last a lifetime and include a cash value component, term life typically offers coverage for a set number of years, making it a more affordable choice for many families. This type of policy allows you to tailor coverage to meet your family's needs during critical times, providing peace of mind without the long-term financial commitment. However, it is essential to evaluate the specific duration and amount of coverage to ensure it aligns with your family's financial goals.

On the other hand, other policies such as whole life or universal life insurance may be more suitable for families seeking lifelong coverage and an investment component. These policies accumulate cash value over time, which can be borrowed against or withdrawn, providing a financial resource for emergencies or significant expenses. When deciding between term life insurance and other options, consider factors such as your family's long-term financial needs, budget, and whether you want a policy that builds cash value. Ultimately, understanding your family's unique situation will help you make the best choice for safeguarding their future.